All amounts are in USD unless stated otherwise

- Feasibility Study reflects optimized development plan and current cost environment

- After-tax NPV5% of $622 million and after-tax IRR of 24% at $1,600/oz gold price

- 10.5-year mine life with average annual gold production of 174,700 ounces at AISC of $681/oz

- Years 1-5: Average annual gold production of 196,200 at AISC of $666/oz

- A 12% increase in mineral reserves to 2.0 million gold ounces

- A 7% increase in initial capital to $458 million and 44% decrease in sustaining capital to $83 million, resulting in an overall 4% decrease in LOM capital costs to $564 million

- Launch of project financing process targeting 60% to 70% from non-equity sources, with target start of construction in mid-2022

- Well-funded with $58 million of cash and $27 million of in the money warrants maturing in Q2-22i

BROSSARD, QC / ACCESSWIRE / February 9, 2022 / G Mining Ventures Corp. ("GMIN" or the "Corporation") is pleased to announce the results of its 2022 Feasibility Study (the "FS" or the "Study") for the development of its wholly-owned and permitted Tocantinzinho Gold Project, located in Para State, Brazil ("TZ" or the "Project"). The Study replaces the 2019 Feasibility Study (the "2019 FS") completed by Eldorado Gold Corporation ("ELD"), with updated mineral resource and mineral reserve estimates, re-sequenced mine plan, refined mill designs, and updated current capital and operating cost estimates.

The FS confirms robust economics for a low cost, large scale, conventional open pit mining and milling operation, with industry leading operating costs and high rate of return. The Study outlines total gold production of 1.8 million gold ounces over 10.5 years, resulting in an average annual gold production profile of 174,700 ounces with an All-In-Sustaining Cost ("AISC") per ounce of $681. The Project after-tax net present value ("NPV") (5% discount rate) is $622 million with an after-tax internal rate of return ("IRR") of 24% at a gold price of $1,600 per ounce, and $833 million and 29% at a spot gold price of $1,800 per ounce.

Louis-Pierre Gignac, President & Chief Executive Officer of GMIN, commented: "The Feasibility Study builds on previous technical work while incorporating several improvements and optimizations, notably to the pit design, production schedule, process plant design and support infrastructures. The capital and operating cost estimates rely on recent budgetary quotes reflecting the current cost environment and our project execution approach. Our procurement strategy is to favor sourcing from in-country manufacturers where possible to maximize local benefits and benefit from simplified logistics. The Project provides an attractive gold production profile of approximately 175,000 ounces per year over a 10.5 year mine life, making it one of the premier gold development projects in Brazil and a key socio-economic contributor to the Tapajos Region of Para State. Factoring recent inflationary pressure seen within the industry from a new project perspective, GMIN has delivered a study that highlights a very attractive rate of return. Our experience and expertise, proven in recent successful mine developments for Newmont and Lundin Gold, will play a key role as capital is deployed to deliver on these economics."

Table 1: Key Economic Outputs of the Study

Description | Units | GMIN | 2019 FS |

| Production Data (Operations Period) |

| ||

Mine Life | years | 10.5 | 10.0 |

Average Milling Throughput | tpd | 12,587 | 11,890 |

Average Milling Throughput | MMt / year | 4.6 | 4.3 |

Strip Ratio | waste : ore | 3.4 | 3.7 |

| Pre-Strip Tonnage | Mt | 17.1 | 22.7 |

| Total Tonnage (exclusive of pre-strip) | Mt | 194.9 | 164.6 |

| Ore Tonnage Milled | Mt | 48.3 | 40.0 |

Gold Head Grade | g/t | 1.31 | 1.41 |

Contained Gold | koz | 2,036 | 1,817 |

Recovery | % | 90.1% | 89.5% |

Total Gold Production | koz | 1,834 | 1,625 |

Average Annual Gold Production | koz | 175 | 163 |

| First Five Full Years | koz | 196 | 187 |

| Operating Costs (Average LOM) |

| ||

Mining Cost | USD/t mined | $2.36 | $2.77 |

Mining Cost | USD/t milled | $9.51 | $11.41 |

Processing Cost | USD/t milled | $8.83 | $9.03 |

G&A Cost | USD/t milled | $3.13 | $2.99 |

Total Site Costs | USD/t milled | $21.48 | $23.43 |

Total Site Costs | USD/oz | $565 | $577 |

| Total Operating Costs / Cash Costs | USD/oz | $623 | $633 |

| AISC | USD/oz | $681 | $735 |

| Capital Costs |

| ||

Initial Capital | USD MM | $427 | $400 |

Life of Mine Sustaining Capital | USD MM | $71 | $129 |

Closure Costs | USD MM | $24 | $27 |

Capital Costs before Tax | USD MM | $522 | $556 |

Net Taxes Payable | USD MM | $42 | $35 |

Total Capital Costs | USD MM | $564 | $590 |

| Financial Evaluation |

| ||

Gold Price Assumption | USD/oz | $1,600 | $1,500 |

USD:BRL FX Assumption | x | 5.20 | 4.00 |

After-Tax NPV5% | USD MM | $622 | $409 |

After-Tax IRR | % | 24.2% | 19.7% |

Payback | Years | 3.2 | 3.4 |

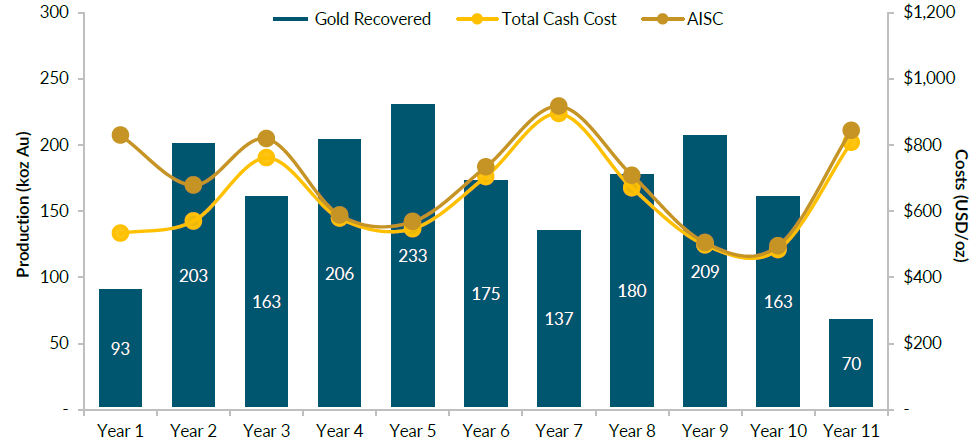

Figure 1: Average Annual Gold Production and Operating Costs

Table 2: Sensitivity Analysis

| Scenario | Downside | Base | Spot | Upside | |

| Gold Price | USD/oz | $1,400 | $1,600 | $1,800 | $2,000 |

| After-Tax NPV5% | USD MM | $410 | $622 | $833 | $1,044 |

| After-Tax IRR | % | 19% | 24% | 29% | 34% |

| LOM Free Cash Flow | USD MM | $744 | $1,043 | $1,343 | $1,642 |

| LOM EBITDA | USD MM | $1,437 | $1,792 | $2,147 | $2,502 |

| Payback | Years | 3.7 | 3.2 | 2.7 | 2.3 |

FS Overview

The Corporation retained G Mining Services Inc. ("GMS") and SRK Consulting Canada Inc. ("SRK") as lead consultants, along with other engineering consultants, to complete the Study and prepare a technical report in compliance with National Instrument 43-101 Standards of Disclosure for Mineral Projects ("NI 43-101").

Property Description, Location, and Access

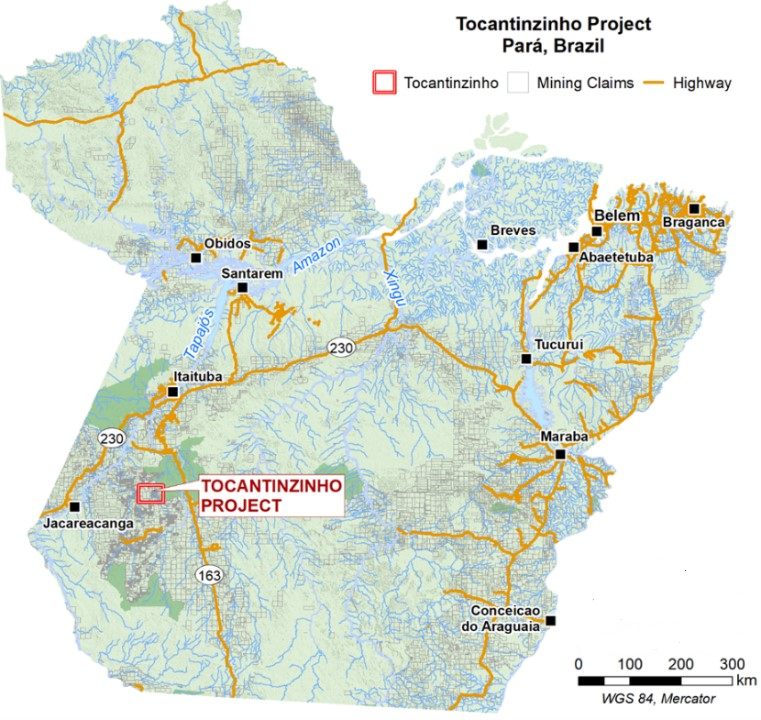

The Project is an advanced-stage development gold project located in Pará State, Brazil, 200 km south-southwest of the city of Itaituba, 108 km from the Moraes de Almeida district, and 1,150 km southwest of Belém, capital of Pará State. The climate in northwestern Brazil is tropical, with a rainy season from January to April and a dry season extending from June to December. The average annual precipitation is approximately 1,957 mm. The land tenure totals 99,574 hectares (996 km2) and is comprised of two mining concessions covering an area of 12,889 hectares (129 km2), 23 exploration licenses covering an area of 76,116 hectares (761 km2), and two applications for exploration licenses covering 10,569 hectares (106 km2).

The Project is accessible by road via a 72-km municipal dirt road connecting to the Transgarimpeira State Road which connects to the Federal BR-163 Cuiaba-Santarem paved highway; the dirt road was built by ELD prior to the sale of the Project. Air access is via an existing 775m long airstrip; a new 1,300m long airstrip capable of landing larger planes is planned that will be used for personnel, priority supplies, medical emergencies and exporting gold. At the Project site, there is an existing exploration camp with a capacity of about 90 beds complete with kitchen, recreation room, clinic, fuel storage, core shacks, and office space.

Figure 2: Project Location Map

Mineral Resource Estimate

Measured and Indicated Resources ("M&I") total 48.1 million tonnes ("Mt") at an average gold grade of 1.36 grams per tonne ("g/t") for 2,102,000 contained ounces of gold (inclusive of Mineral Reserves) as of December 10, 2021. Contained gold in the M&I category represents 97% of the global resource. The Mineral Resource Estimate for the Project is effectively unchanged from the estimate incorporated into the 2019 FS. SRK was commissioned to audit the mineral resource model prepared in the 2019 FS, to audit the surface garimpeiro tailings mineral resource model prepared by GMS (2021), and to assume the Qualified Person responsibility for these mineral resource models.

The mineral resource model only considers work completed by previous operators and consists of 78 core boreholes (22,134 metres) drilled during February 2004 to September 2008, and 74 core boreholes (22,030 metres) drilled during September 2008 to December 2010. In addition, some 155 tailing boreholes (1,594 metres) drilled in 2011 and 2014 were considered for the tailings mineral resource model.

Table 3: Mineral Resource Estimate

| Classification | Tonnes | Grade Gold | Contained Gold |

| Measured | 17,609 | 1.49 | 841 |

| Indicated | 30,505 | 1.29 | 1,261 |

| Total M+I | 48,114 | 1.36 | 2,102 |

| Inferred | 1,580 | 0.99 | 50 |

Note: Mineral resources are not mineral reserves and have not demonstrated economic viability. All figures are rounded to reflect the relative accuracy of the estimates. Assays were capped where appropriate. Open pit mineral resources are reported at a cut-off grade of 0.30 g/t gold. The cut-off grades are based on a gold price of US$1,600 per troy ounce and metallurgical recoveries of 78% for gold in saprolite rock, 90% for gold in granite fresh rock, and 82% for gold in artisanal miner tailings. Effective date of this estimate is December 10, 2021. | |||

Mineral Reserve Estimate

The Project mine plan is based on Proven and Probable Mineral Reserves of 48.7 Mt at an average gold grade of 1.31 g/t for 2,042,000 contained ounces of gold as of December 10, 2021. The contained gold in the proven category represents 41% of the total ore reserve estimate, and the Mineral Reserves almost represent 100% of the Mineral Resource. The saprolite and garimpeiro tailings represent only 5% of the ore reserve contained gold (or 6% of tonnage) with the granite fresh rock being the main material type at 95% of contained gold (or 94% of tonnage).

The Proven and Probable ore reserves are inclusive of mining dilution and ore loss. The external mining dilution around the ore blocks results in a dilution tonnage of 2.6 Mt @ 0.11 g/t, entailing a mining dilution of 5.5%.

For mine planning purposes, GMS built a sub-blocked model for the tailings and the contact between the models using a SMU block size of 1 m x 1 m x 1 m and the remainder of the orebody using a SMU block size of 10 m x 10 m x 10 m in line with a bulk mining approach and appropriate to the style of mineralization.

Table 4: Mineral Reserve Estimate

| Classification | Tonnes | Grade Gold | Contained Gold |

| Proven | 17,973 | 1.46 | 842 |

| Probable | 30,703 | 1.22 | 1,200 |

| Total P&P | 48,676 | 1.31 | 2,042 |

Notes: CIM definitions were followed for mineral reserves. Mineral reserves are estimated for a gold price of $1,400/oz. Mineral reserve cut-off grade of 0.36 g/t. A dilution skin width of 1 m was considered resulting in an average mining dilution of 5.5%. Bulk density of ore is variable with an average of 2.67 t/m3. The average strip ratio is 3.4:1/ Numbers may not add due to rounding. Effective date of this estimate is December 10, 2021. | |||

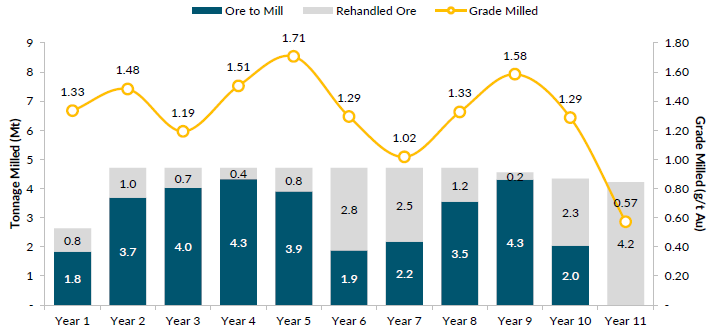

Production Profile

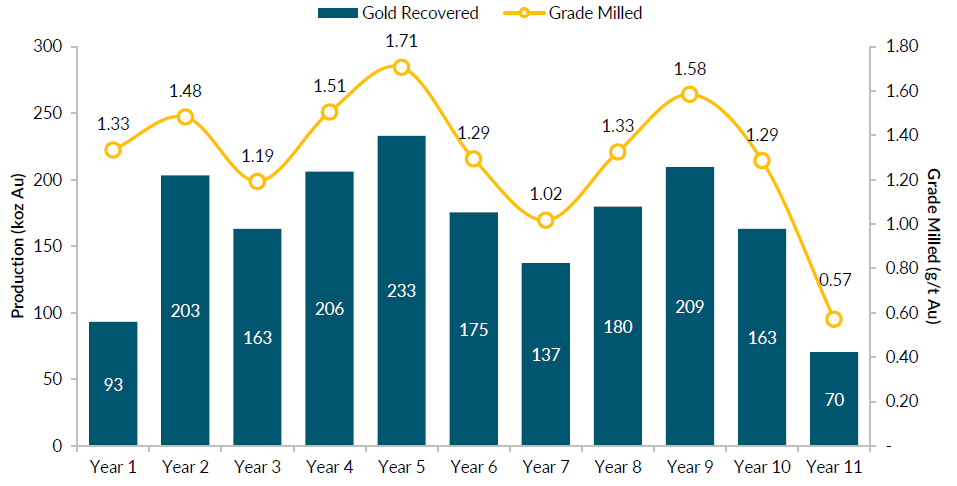

The Study outlines an average annual gold production profile of 174,700 ounces over the 10.5 years of mine life, with Year 1 as partial year considering 6 months of commercial production. Total gold production is 1,838 koz with an average gold grade milled of 1.31 g/t, and metallurgical recovery of 90%. Included in this total is 4 koz of gold recovered during pre-production with the balance of 1,834 koz during commercial production.

Figure 3: Gold Production Profile

| Year | Year | Year | Year | Year | Year | Year | Year | Year | Year | Year |

| Ore Milled (kt) | 2,236 | 4,705 | 4,705 | 4,705 | 4,705 | 4,705 | 4,705 | 4,705 | 4,552 | 4,340 | 4,222 |

| Grade Milled (g/t) | 1.47 | 1.48 | 1.19 | 1.51 | 1.71 | 1.29 | 1.02 | 1.33 | 1.58 | 1.29 | 0.57 |

| Contained Gold (koz) | 106 | 224 | 180 | 228 | 258 | 196 | 154 | 201 | 232 | 180 | 78 |

| Recovery | 88% | 91% | 90% | 90% | 90% | 90% | 89% | 90% | 90% | 91% | 91% |

| Gold Recovered (koz) | 93 | 203 | 163 | 206 | 233 | 175 | 137 | 180 | 209 | 163 | 70 |

Mining

Mining is contemplated as a conventional open pit operation using 16.5 m3 hydraulic excavators and fleet of 92 t mine trucks. A bulk mining approach is well suited for the massive ore body with mining to take place on 10 meter ("m") high benches. The mine is planned as an owner mining operation with blasting activities to be outsourced.

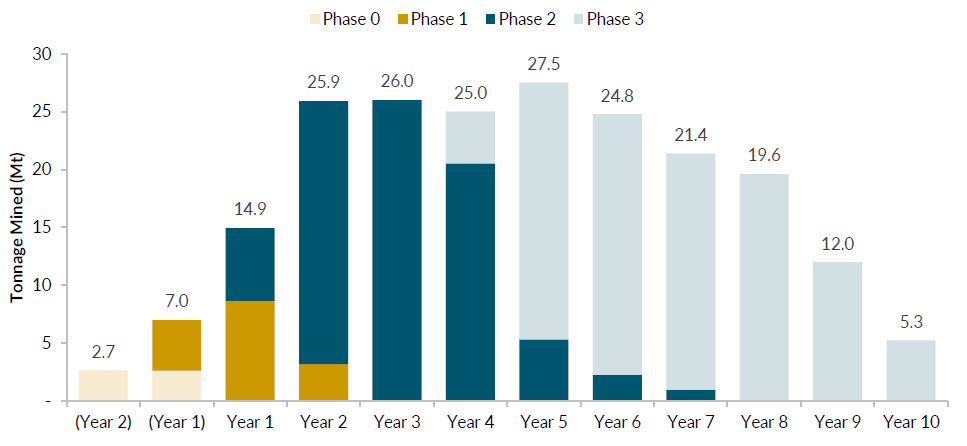

The mine consists of a single open pit that will be developed in four phases, which allows for deferral of waste stripping over the mine life and maximizing mill feed grade during the earlier years with an objective of optimizing the production schedule and resulting economics.

Table 5: Mining Physicals Summary by Phase

| Summary by Mining Phase | Unit | Total | Phase 0 | Phase 1 | Phase 2 | Phase 3 |

| Length of Phase | years | 11.0 | 1.0 | 1.3 | 3.4 | 5.3 |

| Strip Ratio | W:O | 3.4 | 2.1 | 1.3 | 2.6 | 5.4 |

| Total Tonnage | kt | 212,067 | 5,273 | 16,220 | 84,166 | 106,407 |

| Waste Tonnage | kt | 163,391 | 3,576 | 9,135 | 60,788 | 89,891 |

| Rock Tonnage | kt | 133,185 | 2,021 | 5,237 | 47,513 | 78,415 |

| Saprolite Tonnage | kt | 29,715 | 1,474 | 3,644 | 13,122 | 11,475 |

| Tailings Tonnage | kt | 491 | 81 | 254 | 153 | 2 |

| Ore Tonnage | kt | 48,676 | 1,697 | 7,085 | 23,378 | 16,516 |

| Gold Grade | g/t Au | 1.31 | 1.00 | 1.41 | 1.30 | 1.30 |

| Contained Gold | koz | 2,042 | 55 | 320 | 979 | 688 |

Pre-production mining will take place over a period of two years with a total of 17.1 Mt mined, which will provide for waste fill material for construction purposes and will expose higher grade ore prior to commercial production. The ore mined during pre-production will be stockpiled. A maximum 8.9 Mt of stockpiled ore is planned at peak capacity. This material will be stockpiled to cover periods of increased stripping and to match blending requirements for the mill. At the start of commercial production, a stockpile of 4.1 Mt is planned to be available containing 165,000 gold ounces at a gold grade of 1.24 g/t.

Figure 4: Mineral Stockpile Inventory

The open pit will generate 163.4 Mt of waste rock and 48.7Mt of ore, inclusive of historic garimpeiro tailings, over the life of mine ("LOM") for an average LOM strip ratio of 3.4:1. Mining activities are planned over a duration of 11 years which includes 2 years of pre-production mining. Once the open pit is depleted and activities are stopped, stockpile reclaim continues for another 1.5 years to feed the mill. The mining rate reaches a peak of 27.5 Mt/y in year 5 of production.

Figure 5: Annual Mine Production

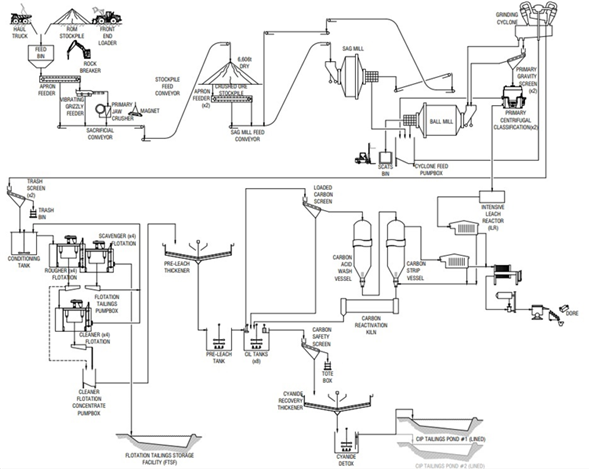

Processing and Recovery

TZ ore contains two types of gold associated with sulfide minerals; the first association occurs with pyrite, while the second association exists with pyrite, chalcopyrite, galena and sphalerite. The conventional process plant design for the Project is based on a robust metallurgical flowsheet to treat gold bearing ore to produce doré. The process plant is designed to nominally treat 4.34 Mt of granite ore per year and will consist of comminution, gravity concentration, gold flotation, cyanide leach and adsorption of the gold concentrate via carbon-in-leach ("CIL"), carbon elution and gold recovery circuits. CIL tailings, representing 5% of tails, will be treated in a cyanide destruction circuit and dewatered to produce a tailings slurry for storage in geomembrane lined ponds. The bulk of the tailings (95%) from the flotation circuit are inert and disposed in a separate facility.

Figure 6: Process Flowsheet

The mill schedule includes two months of commissioning with ore with the second month planned to achieve 60% of nameplate capacity after which commercial production will be achieved with 10.5 years of operation. The peak milling capacity is 4,705 kt/y or 12,890 t/d of nominal throughput and is maintained for the first 7.5 years while softer saprolite and tailings material is available as "supplemental" mill feed at a rate of 1,000 t/d in addition to the fresh rock. Fresh rock will represent 94% of the total mill feed with saprolite and tailings representing only 6%. Mill feed will be maximized with direct feed from the pit and rehandled stockpiled material. The average annual plant head grade is detailed below in Figure 7. The combined average annual plant feed grade is 1.31 g/t Au with a maximum peak of 1.71 g/t Au in Year 5.

Figure 7: Annual Mill Production

Table 6: Metallurgical Recoveries

| Material | Grade | Total | Mill |

| Granite | 1.32 | 91% | 94% |

| Saprolite | 1.03 | 71% | 3% |

| Garimpeiros Tailings | 1.11 | 85% | 3% |

| Total LOM | 1.31 | 90% | 100% |

Power

Power is to be supplied from the Novo Progresso substation to the south, which will require the construction of a 198km 138 kV transmission line and a substation at the site. The Installation License ("LI") for the transmission line was granted in 2017. The new line will be parallel to the Federal highway 163 towards Moraes Almeida, then will turn west along the site access road and eventually connect to the site substation adjacent to the plant site. Average power consumption is estimated at 20 MW with a peak requirement of 24 MW. Emergency diesel generators will provide 6.2MW of backup for critical loads as required in the event of a loss of utility power. The capital cost of the transmission line is included in the FS.

Environmental and Permitting

Environmental studies were completed by the previous owner and the major permits required for construction were granted as follows:

- Para State Department of Environment and Sustainability granted the LIs in April 2017, which were later modified in August 2017, and are comprised as follows:

- Tocantinzinho Site

- Tailings Dam and CIP Pond

- Transmission Line

- Landfill

- Fuel Station

- Concrete Batch Plant

- National Department of Mineral Production (renamed National Mining Agency) issued the mining concessions in May 2018.

Due to competing corporate priorities, the previous owner was not prepared to move the Project to a construction phase and as a result requested that the LI's be frozen for a period of two years. Promptly following GMIN's acquisition of the Project, administrative initiatives were undertaken to unfreeze the LIs in order to meet the planned construction schedule targeted to commence in mid-2022. Additionally, GMIN has requested a two-year extension to the validity of the LI's.

Operating Costs

LOM operating costs are estimated at $565 per ounce of gold produced, or $21.48 per tonne of ore processed, as summarized below. The average LOM mining cost is $2.36 per tonne mined. The LOM AISC is estimated to be $681 per ounce of gold produced based on average annual gold production of 174,700 ounces over the 10.5 years of mine life, which places the Project in the bottom quartile of the global gold cost curve.

Table 7: Operating Cost and AISC Summary

Mining Cost Summary | Total (USD MM) | Unit Cost (USD/t milled) | Cost per oz (USD/oz) |

| Mining | $459 | $9.51 | $250 |

Processing | $427 | $8.83 | $233 |

G&A | $151 | $3.13 | $82 |

Total Site Costs | $1,037 | $21.48 | $565 |

Transport & Refining | $18 | $0.38 | $10 |

Government Royalty (1.5% GOR) | $44 | $0.91 | $24 |

Private Royalty (1.5% NSR) | $44 | $0.91 | $24 |

Total Operating Cost / Cash Costs | $1,143 | $23.68 | $623 |

Sustaining Capital | $83 | $1.72 | $45 |

Closure Costs | $24 | $0.49 | $13 |

AISC | $1,250 | $25.88 | $681 |

Note: Total Cash Costs and AISC are non-GAAP measures and includes royalties payable. | |||

Project Royalties

The Study considers two royalties on the Project:

- Federal Government Royalty: 1.50% of gross sales of the mineral product.

- Private Royalty: 1.50% of net smelter return of the mineral product.

The economic analysis assumes GMIN's exercise of a buydown right for a cash consideration of $3.5 million at the beginning of the construction period, thus reducing the Private Royalty from its current rate of 2.50% to 1.50%. The buydown right is not included in the costs; however, it is included in the economic analysis calculations.

Capital Cost Estimates

The initial capital cost is estimated to be $458 million, which is inclusive of $38 million of contingency (10% before taxes), and $31 million of taxes. The initial capital cost is presented in US dollars using an exchange rate of 5.20 BRL/USD, with an estimated 54% to be spent in the BRL currency. The total construction period is 29 months.

To capitalize on Brazil's domestic manufacturing capabilities, GMS and GMIN visited multiple in-country vendors, equipment suppliers, and contractors in preparation of the updated capital cost estimates. The capital cost estimates are supported by budgetary quotes received in calendar Q4-21, with some of the key items detailed below:

- Multiple equipment vendors provided budgetary quotes for essentially all the mechanical process equipment;

- All major construction bulk material pricing is supported by several in-country vendor quotes;

- Labor costs are fully supported by in-country labor surveys conducted in Q4-21, with input from multiple mining companies, construction companies, and contractors;

- Capital cost for major mining equipment is based on budgetary quotes, with certain units fully negotiated and purchase orders issued;

- 44% of the $42 million required for major mine equipment is committed at this time with firm pricing secured, which includes a portion of the long-lead items required to meet the pre-production schedule;

- Includes twelve 92t mining trucks and a matching hydraulic excavator;

- 44% of the $42 million required for major mine equipment is committed at this time with firm pricing secured, which includes a portion of the long-lead items required to meet the pre-production schedule;

- Three in-country local contractors provided quotes for the 138kV transmission line; and

- Pricing of camp facilities and other support infrastructure are based on multiple bids and are already at the negotiation stage

Sustaining capital is estimated to be $83 million and is inclusive of $12 million of taxes. Over 60% of the sustaining capital spend will be incurred during the first 2 years of production, with the remaining spread equally over the LOM. Less than 40% of the sustaining capital will be spent in the BRL currency. The biggest cost driver of sustaining capital is additional mining equipment ($50 million) and tailings management ($17 million). The flotation tailings facility benefits from favorable topography involving the construction of only one main dam requiring approximately 1.5Mm3 of fill in total for the initial starter dam and subsequent raises to be completed as part of sustaining capital. Fill material will be sourced from the pit resulting in cost synergies.

Closure costs are projected to be $24 million, inclusive of $5 million of contingency (30%). The process plant and some major equipment will have some salvage value after operations, estimated at $13 million, which is excluded from the closure costs but taken into account in the cash flow model.

Table 8: Capital Cost Summary

| Capital Cost Breakdown (USD MM) | Initial Capital | Sustaining Capital | Closure Costs |

Process Plant | $79 | $5 | - |

Power and Electrical | $58 | - | - |

Mining Equipment | $43 | $50 | - |

Infrastructure | $38 | - | - |

Tailings & Water Management | $12 | $17 | - |

Surface Operations | $11 | - | - |

Closure and Rehabilitation | - | - | $18 |

Sub-Total - Direct Costs | $240 | $71 | $18 |

Indirect Costs | $53 | - | - |

Owners Costs | $55 | - | - |

Pre-Production Costs | $41 | - | - |

Contingency | $38 | - | $5 |

Capital Costs Before Tax | $427 | $71 | $24 |

| Net Taxes Payable | $38 | $12 | - |

Total Capital Costs | $458 | $83 | $24 |

Further Optimization, Cost Reductions and Project Potential

The Corporation believes there are potential opportunities to further improve the economics of the Project through the detailed engineering phase and over time:

- Optimization of comminution circuit following additional test work;

- Improved gold recovery with fine grinding of sulphide concentrate prior to leach;

- Increased Mineral Resources and Reserves at depth;

- Exploration success within the large surrounding land package; and

- Additional revenues from silver.

Corporate Update - Launch of Project Financing

The Corporation is formally launching the project financing process, which will be managed internally by Dušan Petković, Vice President, Corporate Development & Investor Relations. Before joining GMIN, Mr. Petković spent 10 years at one of the global leading financiers to the mining sector, where he was Principal, Private Debt, and a member of the investment committee that managed more than 80 investments totaling over $2.5 billion. Mr. Petković was responsible for the origination, structuring, and investment management of bespoke project financing transactions for single-asset emerging producers that included senior and junior debt, commodity linked notes, precious metal streams, and royalties.

The Corporation will be evaluating various sources of funding, including commercial bank debt, private debt, precious metals streaming, and equity, and will work to have the project financing secured to move forward with a construction decision by mid-2022. Targeting 60% to 70% of the capital required from non-equity sources, the key objective is to finance the project, manage risk and volatility, and deliver enhanced IRR and NPV5% attributable to common shareholders.

Timetable and Next Steps

Over the next 12 months, the Corporation will be focused on the following activities:

- Project financing secured by mid-2022;

- Completion and results of 10,000-meter exploration and drilling program in Q3-2022;

- Start of detailed engineering in Q1-2022;

- Start of Project construction by Q3-2022; and

- Expected first gold production in Q3-2024 with first year of full production in 2025.

Conference Call Details

The Corporation is hosting a live webinar on February 10 at 10:00 a.m. Eastern time (7:00 a.m. Pacific time) with the GMIN executive team. All participants are welcome to join and can register in advance through the following link: G Mining Ventures Corp. (TSXV:GMIN) - Feasibility Study Webinar.

After registering, participants will receive a confirmation email containing information about joining the webinar.

Technical Report Preparation and Qualified Persons

The Study has an effective date of December 10, 2021 and was issued on February 9, 2022. It was authored by independent Qualified Persons and is in accordance with National Instrument 43-101 - Standards of Disclosure for Mineral Projects.

GMS was responsible for the overall report and FS coordination, property description and location, accessibility, history, mineral processing and metallurgical testing, mineral reserve estimation, mining methods, recovery methods, project infrastructures, operating costs, capital costs, economic analysis and project execution plan. SRK was responsible for the geological setting, deposit type, exploration, drilling, sample preparation, data verification, mineral resource estimation, environmental studies, permitting and adjacent properties. For readers to fully understand the information in this news release, they should read the technical report in its entirety, including all qualifications, assumptions, exclusions and risks. The technical report is intended to be read as a whole and sections should not be read or relied upon out of context.

The Qualified Persons ("QPs") are Neil Lincoln, P. Eng. having overall responsibility for the Report including metallurgy, recovery methods, capital and operating costs. Camila Passos, MSc, PGeo, CREA-SP of SRK Consulting is responsible for geology and the mineral resource estimate. Charles Gagnon, P. Eng., is responsible for mineral reserves, mining method, capital and operating costs related to the mine. Paulo Ricardo Behrens da Franca, P. Eng. of F&Z Consultoria e Projetos is responsible for tailings management. Thiago Toussaint, MBA, CREA-MG, AMEA of SRK consulting is responsible for environment and permitting.

The technical content of this press release has been reviewed and approved by the QPs who were involved with preparation of the Study. In addition, Louis-Pierre Gignac, President & Chief Executive Officer of GMIN, a QP as defined in NI 43-101, has reviewed the Study on behalf of the Corporation and has approved the technical disclosure contained in this news release. The FS is summarized into a technical report that is filed on the Corporation's website at www.gminingventures.com and on SEDAR at www.sedar.com in accordance with NI 43-101.

About G Mining Services Inc.

GMS a specialized mining consultancy firm based in Brossard, Québec, offering a wide range of services to both underground and open pit mining projects. GMS possesses the capabilities to develop a resource from the exploration phase, to development, into construction, commissioning and then operations. GMS self-performs project development with an objective of building fit-for-purpose and cost effectively. GMS was directly involved in successful construction and development of the Fruta del Norte gold mine in Ecuador (Lundin Gold Inc.) and the Merian gold mine in Suriname (Newmont Mining Corp.), among others. For more information, please visit www.gmining.com.

About G Mining Ventures Corp.

G Mining Ventures Corp. (TSXV:GMIN) is a mineral exploration company engaged in the acquisition, exploration and development of precious metal projects. Its flagship asset, the permitted Tocantinzinho Project, is located in Para State, Brazil. Tocantinzinho is an open-pit gold deposit containing 2.0 million ounces of reserves at 1.3 g/t. The deposit is open at depth, and the underexplored 688km2 land package presents additional exploration potential.

Additional Information

For further information on GMIN, please visit the website at www.gminingventures.com or contact:

Dušan Petković

Vice President, Corporate Development & Investor Relations

416-817-1308

[email protected]

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this press release.

Cautionary Statement on Forward-Looking Information

All statements, other than statements of historical fact, contained in this press release constitute "forward-looking information" and "forward-looking statements" within the meaning of certain securities laws and are based on expectations and projections as of the date of this press release. Forward-looking statements contained in this press release include particularly, but without limitation, those related to the Study results (as such results are set out in the various graphs and tables featured above, and are commented in the text of this press release), such as the Project's production profile, LOM, construction and payback periods, NPV, IRR, (direct/indirect, before/after tax) capital costs, contingency, industry leading operating costs, AISC, sustaining capital costs, free cash flows, mineral proven and probable reserves, M&I resources, open pit ore and waste extraction, mill feed, milling process and recovery, power supply arrangements and power consumption, and closure costs.

Forward-looking statements are based on expectations, estimates and projections as of the time of this press release. Forward-looking statements are necessarily based upon several estimates and assumptions that, while considered reasonable by the Corporation as of the time of such statements, are inherently subject to significant business and economic uncertainties and contingencies. These estimates and assumptions may prove to be incorrect and include, without limitation:

- future price of gold at $1,600 per ounce;

- the USD:BRL foreign exchange rate;

- the USD:CAD foreign exchange rate;

- the various tax assumptions;

- the capital cost estimates being supported by budgetary quotes;

- the labor costs being supported by in-country surveys;

- the project permits' status, notably the timely reinstatement of all necessary LIs, and securing of all other permits and authorizations;

- the exercise of a buydown right to reduce the private royalty to 1.50% of gross sales;

- the securing and proper incurring of the necessary financing to bring the Project into commercial production; and

- all items listed on the above section entitled "Timetable and Next Steps".

Many of these uncertainties and contingencies can directly or indirectly affect, and could cause, actual results to differ materially from those expressed or implied in any forward-looking statements. As future events and results could differ materially what is currently anticipated by the Corporation, notably (but without limitation) in the Study, there can be no assurance that the Study results will prove to be accurate as actual results and future events can differ materially from those anticipated in the Study. Particularly, but without limitation, there can be no assurance that:

- all permits necessary to build and bring the Project into commercial production will be obtained or, as applicable, reinstated;

- the price of gold environment and the inflationary context will remain conducive to bringing a project such as TZ into commercial production;

- outstanding warrants will be exercised and project financing will be secured;

- budgetary quotes will prove accurate;

- the business conditions in Brazil will remain favorable for developing mines such as TZ; and

- the Corporation will bring the Project into commercial production and that it will acquire any other significant precious metal asset.

Forward-looking statements contained in this press release include, without limitation, those related to (i) the Project's improvements and optimizations outlined in the Report, (ii) the decrease in LOM capital costs; (iii )the 12% increase in mineral reserves ; (iv) the launch of project financing endeavors with target start of construction in mid-2022 (targeting 60% to 65% from non-equity sources); (v) the Project's robust economics, notably its low cost and high rate of return; (vi) the suitability of a bulk mining approach; (vii) the production schedule optimization (notably through deferral of waste stripping and maximization of mill feed grade in earlier years); (viii) the pre-production mining providing waste fill material for construction; (ix) the Project's simplified logistics and the Corporation's procurement strategy to favor in-country sourcing; (x) the Project being one of the premier gold development projects in Brazil and a key socio-economic contributor; (xi) the Project being in the bottom quartile of the global cost curve for gold projects; (xii) the Corporation's experience and expertise playing a key role to deliver the Project's economics; (xiii) the numerous opportunities for Project's optimization and growth as outlined under the above section entitled "Further Optimization, Cost Reductions and Project Potential"; (xiv) the above section entitled "Timetable and Next Steps"; (xv) the above corporate update regarding the project financing launch; and (xvi) generally, the above "About G Mining Ventures Corp." paragraph which essentially expresses the Corporation's purpose.

By their very nature, forward-looking statements involve inherent risks and uncertainties, both general and specific, and risks exist that estimates, forecasts, projections and other forward-looking statements will not be achieved or that assumptions do not reflect future experience. Forward-looking statements are provided for the purpose of providing information about management's expectations and plans relating to the future. Readers are cautioned not to place undue reliance on these forward-looking statements as several important risk factors and future events could cause the actual outcomes to differ materially from the beliefs, plans, objectives, expectations, anticipations, estimates, assumptions and intentions expressed in such forward-looking statements.

All forward-looking statements made in this press release are qualified by these cautionary statements and those made in the Corporation's other filings with the securities regulators of Canada including, but not limited to, the cautionary statements made in the relevant section of the Corporation's Management Discussion & Analysis. The Corporation cautions that the foregoing list of factors that may affect future results is not exhaustive, and new, unforeseeable risks may arise from time to time. The Corporation disclaims any intention or obligation to update or revise any forward-looking statements or to explain any material difference between subsequent actual events and such forward-looking statements, except to the extent required by applicable law.

i 42.7 million warrants with a strike price of C$0.80 and average life of 0.4 years. Figures converted at USD:CAD FX of 1.25.

SOURCE: G Mining Ventures Corp.