PITTSBURGH, PA / ACCESSWIRE / October 17, 2023 / SSB Bancorp, Inc. (OTCQX:SSBP) (the "Company"), the holding company for SSB Bank (the "Bank"), today announced the Company's unaudited, consolidated results of operations for the three months and nine months ended September 30, 2023.

Total assets increased $39.6 million to $290.8 million at September 30, 2023, from $251.2 million at December 31, 2022. The increase in assets was due to an increase in deposits of $38.0 million as well as a net increase in Federal Home Loan Bank advances of $1.0 million. These funding increases were converted into a net increase of $18.7 million in net loans, $9.9 million in certificates of deposit, and $9.6 million in interest-bearing deposits with other financial institutions.

For the three months ended September 30, 2023

Net earnings for the three months ended September 30, 2023, was $626,000, or $0.29 per basic and diluted share, compared to net earnings of $248,000, or $0.12 per basic and diluted share, for the three months ended September 30, 2022.

Total interest and fee income increased by $1.3 million, or 49.6%, when comparing the results of the three months ended September 30, 2023, to the three months ended September 30, 2022. This is due to the increase in yield of interest-earning assets from 4.57% to 5.29% as well as an increase in average interest-earning assets of $66.0 million when comparing the two periods.

Interest expense increased by $895,000, or 120.0%, to $1.6 million in the three months ended September 30, 2023, from $746,000 in the three months ended September 30, 2022. The increase in interest expense is due to the increase in cost of interest-bearing liabilities from 1.51% for the three months ended September 30, 2022, to 3.16% for three months ended September 30, 2023. This increase in cost is due to the increase in market interest rates when comparing the two periods. Additionally, average interest-bearing liabilities increased by $9.6 million from $198.1 million for the three months ended September 30, 2022, to $207.7 million for the three months ended September 30, 2023.

Noninterest income increased by $221,000, or 74.4%, to $518,000 from $297,000 when comparing the three months ended September 30, 2023, to the three months ended September 30, 2022. The increase is due to the increase in credit card processing fees of $195,000 when comparing the two periods. The credit card processing portfolio continues to grow in both the number of merchants as well as the volume of transactions settled.

Noninterest expense increased by $87,000 or 5.2% to $1.8 million. This was mainly due to an increase in outside professional fees and salaries and employee benefits of $71,000 and $34,000, respectively, when comparing the two periods. These increases were offset by decreases in marketing, occupancy, and FDIC insurance expenses. The decrease in marketing fees reflects a change in business development methods with a higher emphasis on business development through referral of existing business channels.

For the nine months ended September 30, 2023

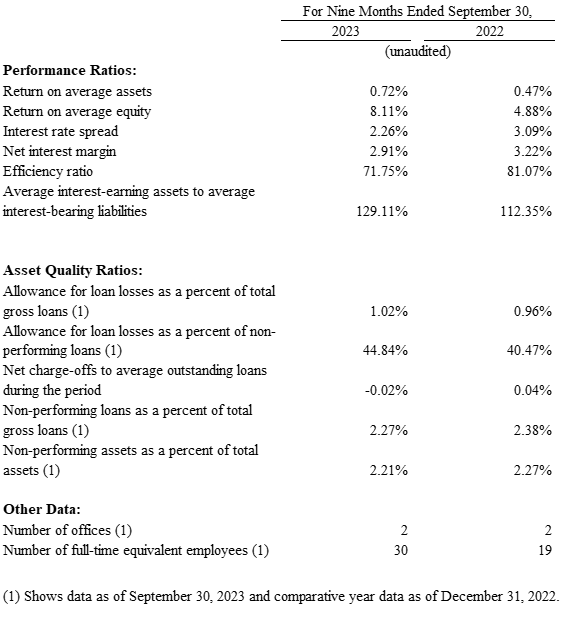

Net earnings for the nine months ended September 30, 2023, was $1.5 million, or $0.71 per basic and diluted share, compared to net earnings of $864,000, or $0.40 per basic and diluted share, for the nine months ended September 30, 2022.

Total interest and fee income increased by $3.1 million, or 43.0%, when comparing the results of the nine months ended September 30, 2023, to the nine months ended September 30, 2022. This is due to the increase in yield of interest-earning assets from 4.31% to 5.12% as well as an increase in average interest-earning assets of $45.6 million when comparing the two periods.

Interest expense increased by $2.6 million, or 144.6%, to $4.5 million in the nine months ended September 30, 2023, from $1.8 million in the nine months ended September 30, 2022. The increase in interest expense is due to the increase in cost of interest-bearing liabilities from 1.23% for the nine months ended September 30, 2022, to 2.86% for nine months ended September 30, 2023. This increase in cost is due to the increase in market interest rates when comparing the two periods. Additionally, there was an increase in the average interest-bearing liabilities of $9.6 million when comparing the two periods.

Noninterest income increased by $638,000, or 76.3%, to $1.5 million from $836,000 when comparing the nine months ended September 30, 2023, to the nine months ended September 30, 2022. The increase is due to the increase in credit card processing fees of $650,000 when comparing the two periods. The credit card processing portfolio continues to grow in both the number of merchants as well as the volume of transactions settled. Additionally, loan servicing fees increased by $42,000 when comparing the two periods. This is due to the slowing of mortgage loan prepayments. Offsetting the increases, gain on sale of loans has decreased when comparing the two periods due to a lower volume of mortgage loan originations in the period.

Noninterest expense increased by $73,000, or 1.5%, to $4.9 million when comparing the nine months ended September 30, 2023, to the nine months ended September 30, 2022. This is due to increases in occupancy, data processing, and contributions and donations. These increases were offset by decreases in salaries and employee benefits, professional fees, FDIC insurance, and marketing expenses. The decrease in salaries and employee benefits is due to a decrease in loan production commissions. The decrease in marketing fees reflects a change in business development methods with a higher emphasis on business development through referral of existing business channels. The increase in data processing expense is due to the increased size and complexity of the Bank's products to service its customers. The increase in contributions and donations is due to an additional Neighborhood Assistance Program contribution that the Bank made to an additional community partner in which the Bank receives PA tax credits in return for the contribution.

This release may contain forward-looking statements within the meaning of the federal securities laws. These statements are not historical facts; rather, they are statements based on the Company's current expectations regarding its business strategies and their intended results and its future performance. Forward-looking statements are preceded by terms such as "expects", "believes", "anticipates", "intends" and similar expressions.

Forward-looking statements are not guarantees of future performance. Numerous risks and uncertainties could cause or contribute to the Company's actual results, performance and achievements to be materially different from those expected or implied by the forward-looking statements. Factors that may cause or contribute to these differences include, without limitation, general economic conditions, including changes in market interest rates and changes in monetary and fiscal policies of the federal government; legislative and regulatory changes.

Because of the risks and uncertainties inherent in forward-looking statements, readers are cautioned not to place undue reliance on them, whether included in this report or made elsewhere from time to time by the Company or on its behalf. The Company assumes no obligation to update any forward-looking statements.

Contact:

Ben Contrucci

CFO

412-837-6955

[email protected]

SOURCE: SSB Bancorp, Inc.